China Strengthens Control Over Africa’s Essential Minerals Amid Global Energy Crisis

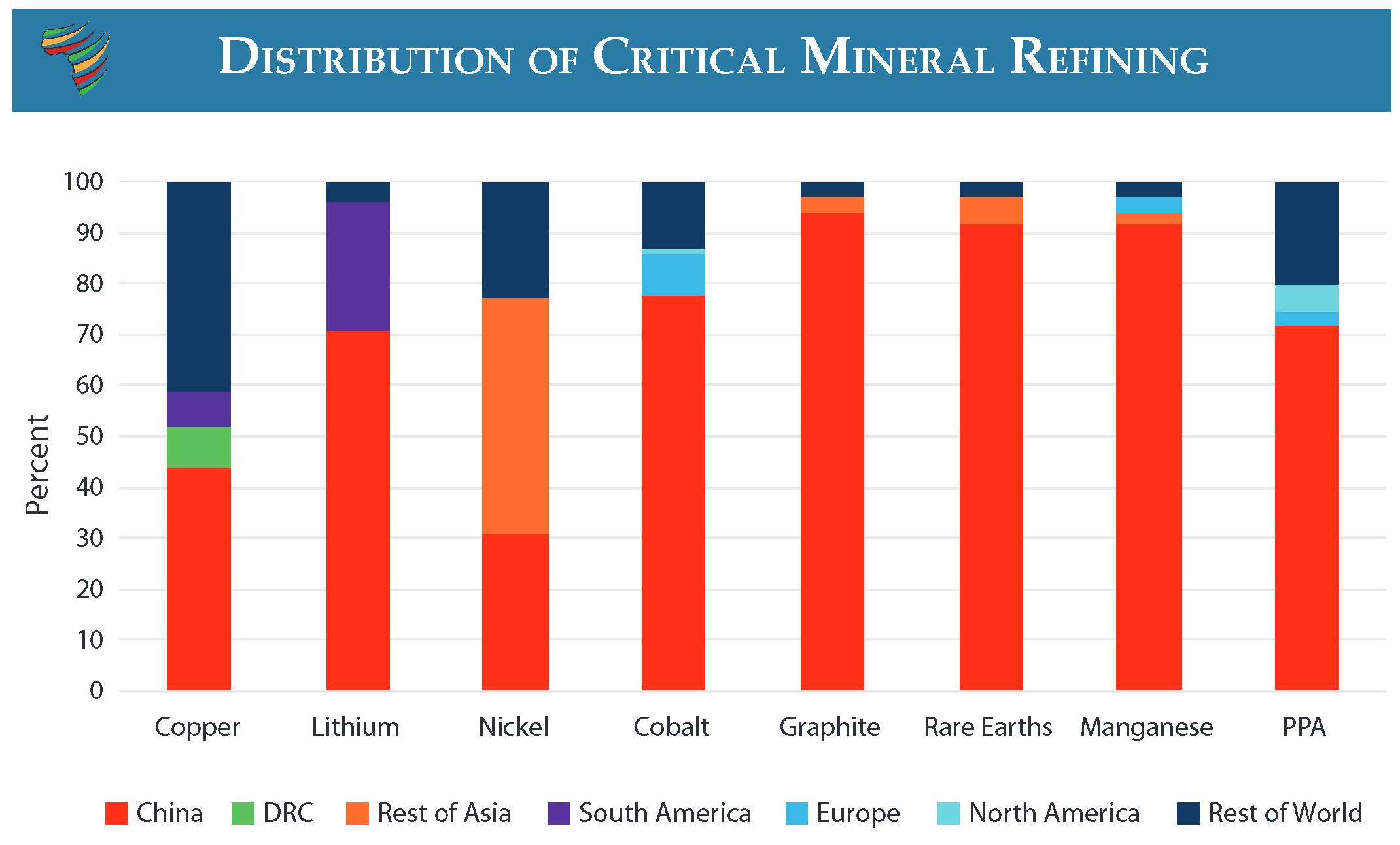

China’s dominance in critical minerals extends far beyond extraction. According to the International Energy Agency (IEA) and the U.S. Geological Survey (USGS), China accounts for a majority share of global rare earth production and as much as 80–90 percent of refining and processing capacity. It also produces roughly 70 percent of rare earth elements and more than 90 percent of high-strength permanent magnets used in electric vehicles, wind turbines, and advanced defence systems.

Africa has become central to this strategy. Chinese firms, backed by state financing, have expanded aggressively into upstream mining assets across the continent. Notable examples include investments in copper in Botswana, lithium in Mali, and rare earth projects in Tanzania. Companies such as BYD have secured multiple lithium concessions to guarantee long-term supply. This expansion is supported by Chinese policy banks, with data from the China Development Bank and the Export-Import Bank of China indicating that nearly $25 billion in mining-related loans were issued in the first half of 2025 under the Belt and Road Initiative framework.

China’s strategic advantage lies in its control of the full value chain; from financing and extraction to logistics and high-value processing. While African countries provide critical raw materials, the most profitable stages of refining and manufacturing remain concentrated in China. According to the World Bank, countries such as the Democratic Republic of Congo, Zimbabwe, Guinea, and Zambia are key suppliers of cobalt, lithium, bauxite, and copper, yet capture limited downstream value.

Beijing has also begun leveraging this dominance geopolitically. In 2025, China introduced tighter export controls on rare earth-related materials and technologies, requiring government approval for certain outbound shipments. Analysts at the Center for Strategic and International Studies (CSIS) and officials within the U.S. Department of the Treasury have warned that such measures could disrupt global supply chains and increase Western dependency on Chinese-controlled inputs.

At the same time, a separate pressure point has emerged in global energy markets. The 2026 escalation in the Middle East, highlighted in reporting by The Washington Post and Reuters, has led to significant disruption in traffic through the Strait of Hormuz, a critical transit route for global oil and gas supplies. According to the U.S. Energy Information Administration (EIA), roughly 20 percent of global petroleum liquids consumption passes through the strait, with a large share destined for Asian markets.

For China, the exposure is significant. The International Energy Agency (IEA) estimates that around 40–50 percent of China’s crude oil imports transit through the Strait of Hormuz. The price shock has been substantial, with Brent crude surpassing $120 per barrel at the height of the crisis, based on market data tracked by major commodity exchanges and reported by Bloomberg.

However, there are certain hinderances. Data from China’s National Energy Administration indicate that strategic petroleum reserves can cover more than 100 days of import demand, providing temporary insulation from supply shocks.

Paradoxically, the disruption has strengthened China’s position in clean energy. As countries accelerate diversification away from fossil fuels, demand for solar, wind, battery, and electric vehicle technologies -sectors where China leads globally- continues to rise. The International Renewable Energy Agency (IRENA) notes that China dominates manufacturing capacity across key clean energy components, reinforcing its central role in the energy transition.

For Africa, this evolving landscape presents both opportunity and risk. While several governments have introduced export restrictions and local beneficiation policies, the African Development Bank (AfDB) has repeatedly highlighted structural gaps in infrastructure, financing, and industrial capacity that limit value addition.

It remains whether African nations can leverage growing geopolitical competition to move beyond raw material exports and secure a stronger position in global supply chains.

0 Comments

No comments yet. Be the first one to comment!